Spoiler Impact Calculator

Premium Impact Estimate

This calculator estimates how a spoiler modification could affect your insurance premium based on industry-standard guidelines.

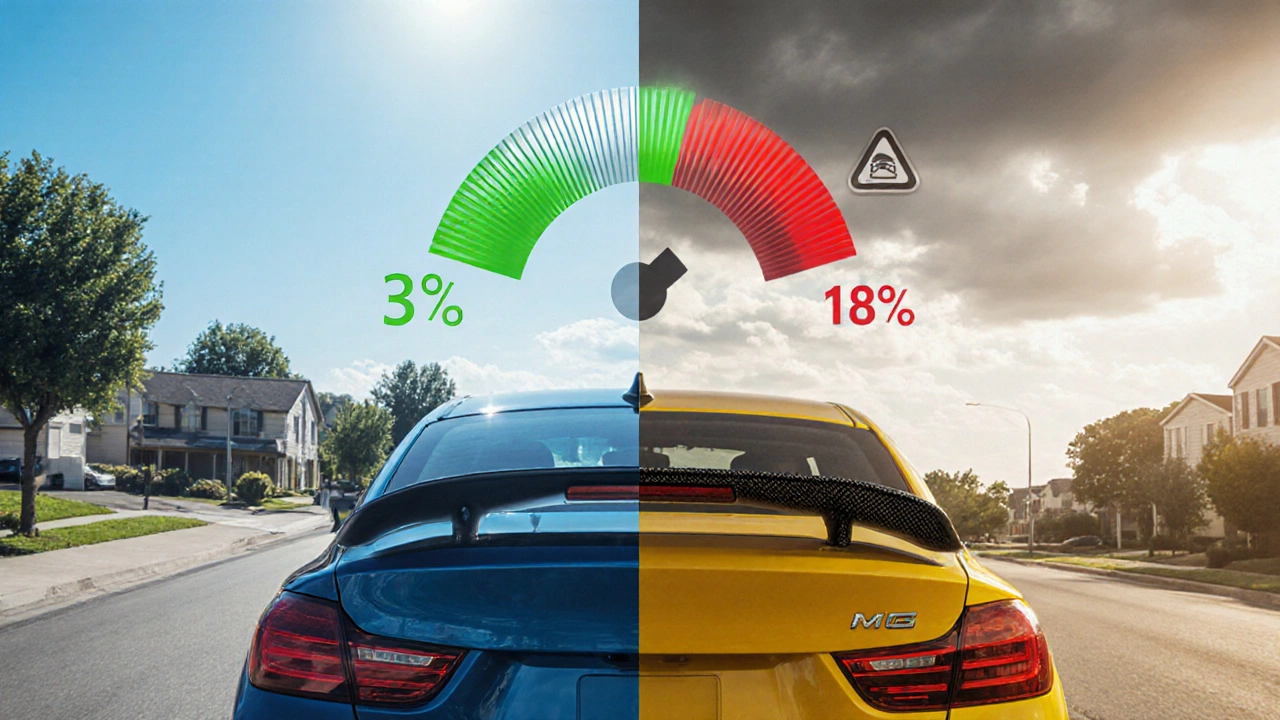

- Factory-Fit Spoilers: Usually cause minimal impact (0-5% increase)

- After-Market Spoilers: May increase premiums by 5-12% if properly reported

- Unreported Modifications: Risk of surcharges up to 20% or policy cancellation

When you’re eyeing that sleek rear Spoiler is a aerodynamic add‑on that can boost downforce, improve handling, and give your car a sportier look. But before you bolt it on, you need to know how it plays with spoiler insurance and whether it will nudge your premiums up or down.

Why Insurers Care About Spoilers

Insurance companies treat any change to a vehicle’s original specifications as a Modification. The underwriting process looks at three risk factors:

- Vehicle value - a spoiler can increase the perceived market value.

- Performance impact - added downforce may enable higher cornering speeds, which some insurers view as a higher accident risk.

- Safety perception - poorly installed parts can lead to structural failure in a crash.

When these factors shift, the insurer may adjust the Premium or request proof that the part meets safety standards.

Common Scenarios and Premium Effects

Below is a quick look at how different spoiler situations typically affect your policy.

| Scenario | Typical premium change | Key considerations |

|---|---|---|

| Factory‑fit spoiler (manufacturer‑approved) | 0‑5% increase or neutral | OEM part, covered by warranty, no extra paperwork |

| After‑market carbon‑fiber spoiler, properly installed and reported | 5‑12% increase | Provide installation receipt, certify compliance with Australian Design Rules (ADRs) |

| After‑market spoiler, not reported | Potential surcharge up to 20% if discovered during claim | Risk of claim denial or policy voiding |

| Removable "bolt‑on" spoiler, reported as optional accessory | 2‑4% increase | Insurer may require proof it’s non‑permanent |

Steps to Keep Your Policy Safe

- Check your current Policy wording for any “modifications” clauses.

- Choose a spoiler that meets Australian Design Rules (ADR 69/00 for aerodynamic devices).

- Hire a qualified installer; ask for a compliance certificate.

- Notify your insurer before the part is fitted. Provide photos, invoices, and the compliance certificate.

- Ask the insurer how the new part will be reflected in your premium and whether any discounts are possible (e.g., for safety‑tested accessories).

- Keep all documentation in a folder for future Claim submissions.

Case Studies From the Road

Case A - Sydney driver, 2023: Installed a carbon‑fiber rear spoiler on a Subaru Impreza without notifying the insurer. After a minor rear‑end collision, the adjuster noted the unreported modification and added a 17% surcharge to the settlement. The driver appealed, but the policy was deemed void for non‑disclosure.

Case B - Adelaide driver, 2024: Purchased an OEM‑approved spoiler for a Mazda 3 and reported it. The insurer increased the premium by 3% but offered a “no‑claims bonus” protection upgrade because the part passed crash‑test verification.

These examples show that honest reporting rarely leads to huge spikes, while hidden mods can cost far more if a claim arises.

Key Takeaways

- Any spoiler that wasn’t part of the original build counts as a Modification.

- Reporting the part and providing compliance proof keeps premiums predictable.

- Unreported spoilers can trigger surcharges up to 20% or even policy cancellation.

- Factory‑fit spoilers usually have minimal impact; aftermarket parts need paperwork.

- Keep all invoices and certificates handy for future Claims.

Frequently Asked Questions

Will a small lip spoiler raise my insurance?

If the lip spoiler is an OEM part and you notify the insurer, the increase is usually under 5%. Without notification, the insurer may treat it as an undisclosed modification and apply a higher surcharge.

Do I need a new Policy after installing a spoiler?

You don’t need a brand‑new policy, but you should request an endorsement that records the spoiler. This keeps the coverage intact and the premium calculation transparent.

Can a spoiler ever lower my premium?

Rarely. Some insurers offer discounts for accessories that improve vehicle stability, but they usually require crash‑test data proving the part reduces accident risk.

What documentation should I keep?

Invoice, installation receipt, compliance certificate (showing the part meets ADR standards), and any correspondence with the insurer confirming the endorsement.

If I sell the car, does the spoiler affect insurance for the new owner?

The new owner will need to disclose the spoiler when arranging their own coverage. The previous owner’s history doesn’t carry over, but the vehicle’s registration will list the modification.